How to create a check with: “No Signature Required?”

Check Drafts and RCC Items:

Check Drafts and RCC Items:

No Signature Required:

How to create a check draft with no signature?

Do banks take checks with no signature?

How can I deposit the draft with no signature?

Are No Signature Required Checks real?

Overview:

Checks with No Signature Required are called check drafts, or Remotely Created Checks [RCCs].

These items are used most prominently by companies who take checks by phone, checks by fax or checks online from customers as payment. No Signature Required check drafts are also used by most banks to generate Bill-Pay Checks on behalf of Online Banking customers.

A check draft is different from an ACH, or electronic transfer, because it uses a real paper check. There are few differences.

The difference between a conventional check and a an RCC or Check Draft:

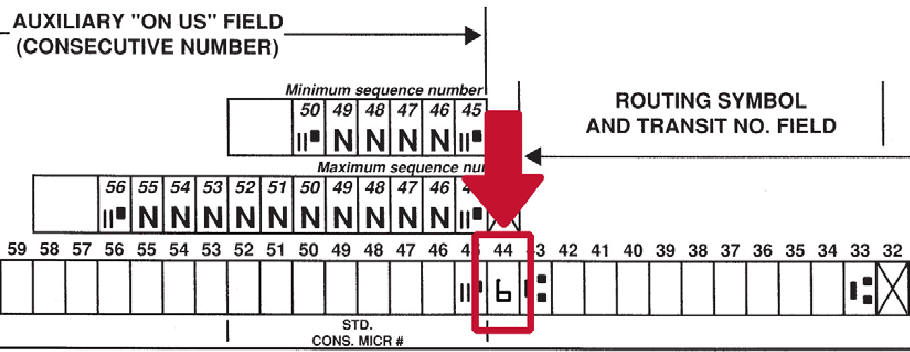

1. The first difference is this number “6” just before the bank routing number.

This called the EPC-6 code, or External Processing Code. The #6 indicates that it is not an original item, signed by the account holder, but that it is a Remotely Created Check [RCC] that is authorized by the account holder.

Regular checks in your checkbook will not have this #6.

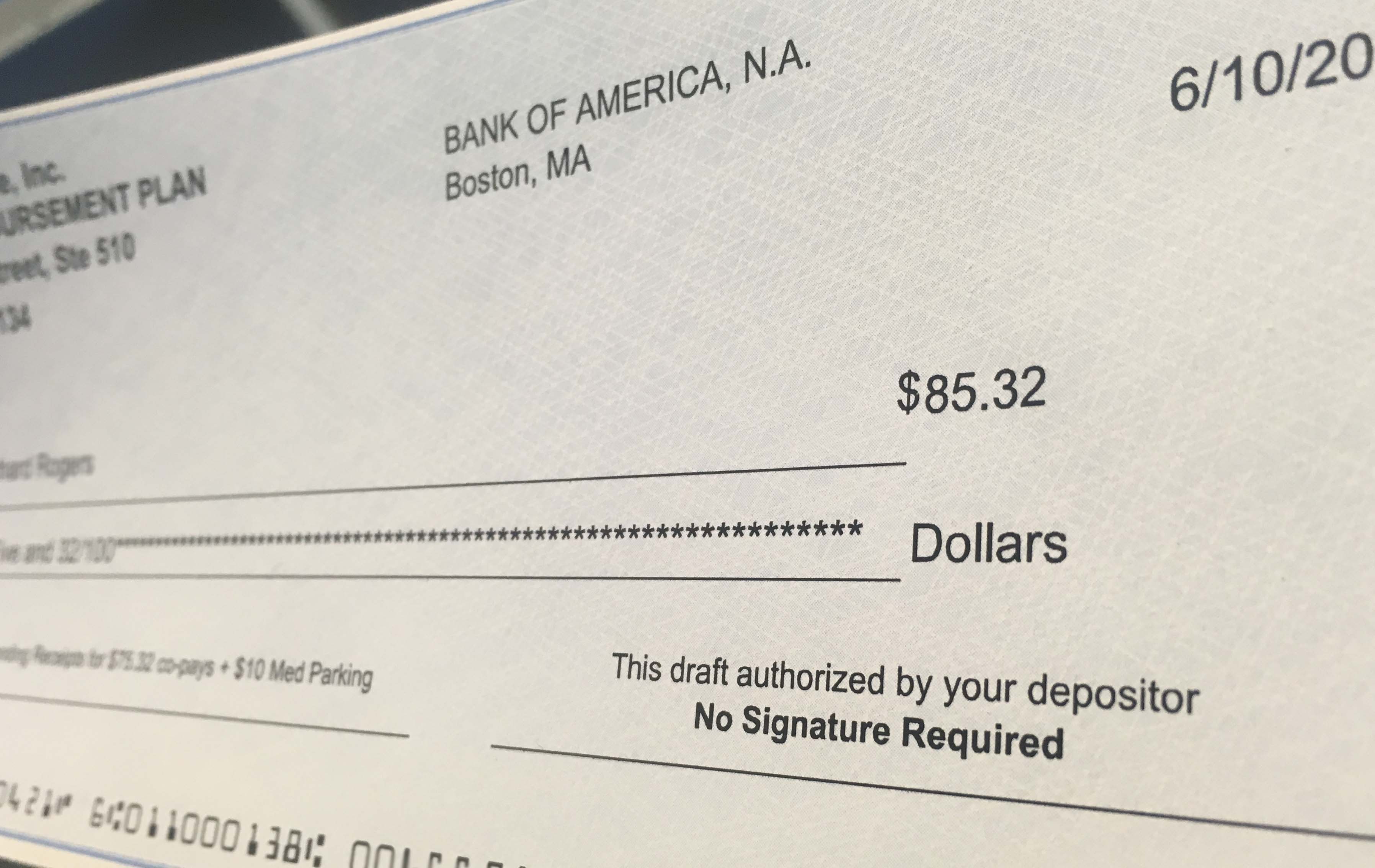

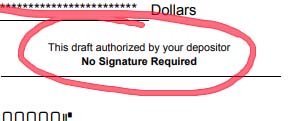

2. There is No Signature Required.

This, or other similar language is used in place of the account holder’s original signature and is accepted for deposit just like a regular check.

CheckWriter™ brand software for printing RCC items and checks by phone, will automatically print a standard signature disclaimer that will be accepted by any bank.

3. Items are typically for deposit only.

In most circumstances, these types of RCC, and not signature required checks are intended for deposit only. Unlike an original, signed check, you may not be able to walk up to the payor’s bank and cash the check at the window.

Conclusion:

Check drafting is simply when a merchant, bank or authorized third party, creates a valid legal copy of the customer’s check with authorization9. Because it is created by the merchant, no signature is required.

More information about Checks vs. Drafts:

It is important to fully understand the language of check acceptance before you begin to deposit drafts or RCC items generated by CheckWriter™ or any other Remote Check Software. With CheckWriter™ software you are accepting the customer’s check information, and creating an RCC or “DRAFT” of their check for deposit.

The Uniform Commercial Code permits the process of drafting by defining signature in the following regulation: Uniform Commercial Code, Title 1, Section 1-201 (39).

This regulation only makes check drafting possible, not “required.” Your bank may deny your items for deposit if they have reason to be suspicious. Suspicious items are covered in Regulation CC 229.13, Exceptions.

Check drafting requires no special license, only the permission of the account holder.

CheckWriter™ will help telemarketers comply with the FTC Regulations 16 CFR 310 in regard to proper record keeping. This regulation only applies to outbound telemarketers, and does not cover inbound calls or transactions between customers where and relationship already exists.

These drafts comply with all known U.S. standards and should only be printed on security bond check paper: Federal Reserve Board of Governors Regulation ‘CC.’

If you approach your bank branch, be sure you word your questions carefully. Most branch managers and tellers do not know much about this technology if their own bank does not provide it, and may even tell you they do not accept such items.

Asking questions of your bank where you raise doubt as to the validity of the items may cause the bank to to hold items under Regulation CC 229.13, Exceptions.

Deposit with confidence. If you create suspicion or doubt about your items, or question their validity to the bank, they may be obligated to freeze the items! Banks take payments of any sort very seriously.